- Employers

- Advisors

ADVISORS

Roundstone recognizes and appreciates the important role benefits advisors play — that’s why we only operate through our network of trusted advisors.

- Resources

THE LATEST AND THE GREATEST

- Blog

BLOG

Stay up-to-date with the latest trends and learn about how small to midsize businesses can enjoy the benefits of self funded health insurance.

LATEST POST

FEATURED FAVORITES

- About Us

ABOUT US

We are a health benefits captive providing self-funded solutions to small and mid-sized employers. Our self-funded medical group captive bands employers together to fund their benefits the way much larger Fortune 500 companies do.

- Our TPA

TOPIC

How to Choose a Provider Network for a Self-Funded Plan

- Roundstone Team

- 8 Minute Read

- Category Here

Find this article helpful? Share it with others.

Network selection is one of the most consequential plan design decisions a self-funded employer makes. It determines where your employees get care, what it costs the plan, and what it costs them out of pocket.

Get it right and it’s one of your most effective cost-containment levers. Get it wrong and it undermines everything else your self-funded plan is designed to do.

Here’s how to get it right.

Is Your Existing Healthcare Plan Sustainable?

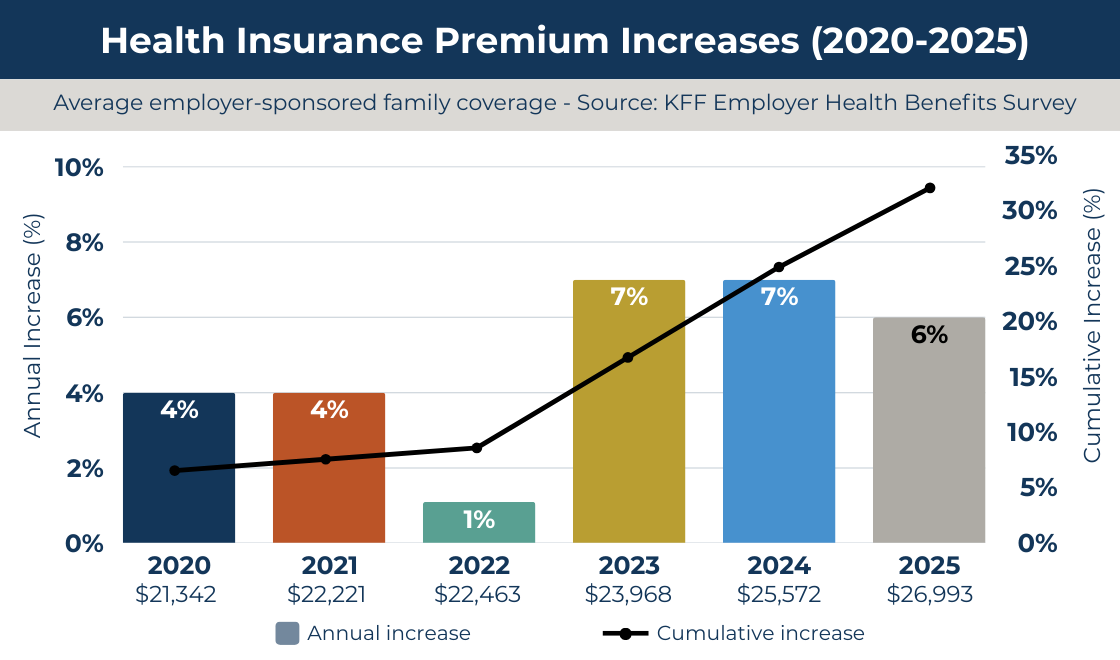

Family premiums for employer-sponsored health insurance reached an average of $26,993 in 2025, according to the KFF 2025 Employer Health Benefits Survey, a 6% increase over the previous year, and more than 26% cumulative growth since 2020.

NOTE: The 2022 dip is a COVID artifact. Delayed and skipped care during the pandemic temporarily suppressed claims, and premiums followed. When utilization rebounded, costs snapped back. The cumulative damage from 2020 to 2025 exceeds 26%.

With a fully insured plan, your network is chosen for you. You absorb cost increases with no idea what’s driving them and no ability to respond.

With a self-funded plan, the network decision is yours. It’s one of the clearest levers you have to directly control what the plan spends.

Know Your Network Options

Network structures differ in cost, access, and administrative complexity. You need to understand the trade-offs before evaluating specific options.

PPOs remain the most common choice. KFF data shows they covered 46% of workers in employer-sponsored plans in 2025. They also tend to be the most expensive option per claim.

Wide access comes with a price, and for self-funded employers focused on cost, that trade-off deserves scrutiny rather than default acceptance.

Other structures, such as HMOs, EPOs, high-performance networks, reference-based pricing arrangements, each offer different cost profiles. The right answer depends on your workforce, not on industry convention.

Benefits advisors: Learn more about self-funding and group captives. Free download.

Match the Network to Your Workforce, Not the Other Way Around

The right network for a 50-person manufacturing company in rural Ohio looks nothing like what works for a 200-person tech firm in a metro area. Your claims data and workforce demographics should drive this decision.

Take all of the following into consideration when choosing your network:

Geography Determines Adequacy

A network with 500,000 providers nationally may have thin coverage within 20 miles of where your employees actually live and work. National numbers are just marketing. What matters is what’s locally available to your employees.

Questions to ask before you sign:

What percentage of your employees live within a defined distance from in-network primary care and specialists?

Does the network include the hospitals your workforce already uses?

Are common specialist types, such as orthopedics, cardiology, and behavioral health, well represented in your area?

Network adequacy is a real and growing problem. The Business Group on Health’s 2025 Employer Health Care Strategy Survey found that 79% of employers cite access as one of their top three mental health priorities, a signal that coverage alone is not enough if the right providers aren’t reachable.

Your Claims History Tells You What the Network Needs to Cover

A younger, relatively healthy workforce will use primary care and urgent care heavily. An older workforce depends on chronic disease management and specialist access. Your claims data tells you exactly which services your employees actually use.

If your prior plan data shows high ER utilization, a network with strong urgent care and telehealth options will cut that cost more effectively than adding more hospitals. If specialty care is a consistent cost driver, verify that your top-used specialties are well-represented before committing to any network.

Roundstone Reporting gives group captive members direct access to that data. Use it.

Negotiate on Rate, Not on Access

Two networks may both claim to cover a region. Their negotiated rates for the same procedure can differ by 30% or more. Network selection without rate evaluation is an incomplete decision.

Benchmark Against Medicare, Not Billed Charges

When evaluating networks, ask for reimbursement data on your most common claim types — but don’t let vendors compare against billed charges. Billed charges are arbitrary and easily manipulated. A 40% discount off an inflated number is not a bargain. Benchmark against Medicare rates for equivalent services. That’s a stable, objective comparison that tells you what you’re actually paying.

For context, Aon’s 2025 Employer Health Cost Assessment projects average plan costs per employee exceeding $16,000 in 2025. Self-funded employers who negotiate stronger network rates can directly move that number. Employers on fully insured plans absorb it.

Join Our Newsletter

Sign up for fresh insights straight to your inbox.

Your PBM Is Either Working for You or Against You

Pharmacy costs are now the fastest-growing line item in most employer health plans, and the reason is usually the same: a pharmacy benefit manager whose incentives don’t align with yours.

Traditional PBMs make money through spread pricing, the difference between what they charge your plan and what they actually pay the pharmacy. That spread is invisible to you by design. You see a net number; you don’t see what’s underneath it.

In a self-funded plan built on transparency, that’s a structural contradiction you can’t afford to ignore.

Pass-through or transparent PBMs operate differently. They pass the actual drug cost and dispensing fee to the plan and charge a flat administrative fee instead. You see every transaction at cost.

That visibility alone changes behavior, and it’s one reason Roundstone’s Preferred Bundle specifies transparent PBMs rather than leaving the choice open.

Specialty drugs and GLP-1 weight loss medications make this even more consequential. They now represent more than 50% of drug spend in many plans, and without full cost visibility, those costs are effectively unmanaged.

Without a PBM that gives you full cost visibility and a formulary strategy built around your actual use, those costs are effectively unmanaged.

When evaluating PBMs alongside your network, ask these questions: Is this a pass-through model or a traditional spread-pricing model?

What is the actual ingredient cost versus what the plan pays?

How does the formulary handle specialty drugs and high-cost categories like GLP-1s?

The answers tell you whether your PBM is a cost-containment partner or a cost-amplifier.

Don't Trade Cost for Quality

A cheaper network that steers employees toward poor-quality care is a cost-shifting, rather than cost-containment strategy. Look for networks that incorporate quality metrics: readmission rates, patient satisfaction scores, and evidence-based practice compliance.

High-performance networks and Centers of Excellence arrangements reduce cost on major procedures while improving outcomes. They exist simultaneously, and you should demand both.

The Self-Funded Advantage: You Can Actually Choose

Fully insured employers accept whatever network their carrier provides. Self-funded employers can access multiple networks, carve out specific services to specialized vendors, and switch partners without rebuilding the underlying plan.

This flexibility has real value. If your current network underperforms, you can correct it. You can add a Centers of Excellence network for high-cost procedures. You can layer a direct primary care contract on top of a broader network. You can also apply reference-based pricing for certain claim categories while maintaining traditional network access elsewhere.

None of that is available on a fully insured plan.

The Roundstone Preferred Bundle: A Proven Starting Point

For employers who want a high-performing, pre-evaluated option, Roundstone’s Preferred Bundle pairs the Cigna national network with Bywater, our in-house third-party administrator (TPA), and select transparent PBMs. It’s a coordinated solution built for cost containment.

Members on the Preferred Bundle average $1,700 less per employee annually compared to other vendor arrangements. That result is driven in part by network selection: a high-performing national network combined with transparent data tools that show exactly where claims spending is going and why.

Employers who want to bring their own network can do that, too. Roundstone’s model supports plan design flexibility. The network choice belongs to the employer.

A Practical Network Evaluation Sequence

Network selection might seem overwhelming, but you can narrow the process quickly with a structured process.

Start with your claims data. If you're coming from a fully insured plan, request your aggregate claims history. If you're already self-funded, use Roundstone Reporting to identify your top 10 procedure categories, most-used specialists, and highest-cost facilities. These form your network requirements.

Map geography against your workforce. Run a zip code analysis to confirm that candidate networks provide adequate access where your employees actually live.

Request rate comparisons on your specific procedure codes. Ask networks for reimbursement data benchmarked against Medicare, not billed charges.

Evaluate telehealth and behavioral health specifically. These are frequently the weakest spots in otherwise strong networks, and they account for a growing share of claims.

Check provider stability. A network that loses key providers mid-year creates disruption and out-of-network exposure. Ask for retention metrics before you commit.

Model the cost impact. Work with your TPA and advisor to project total plan cost under each network option using your actual utilization patterns, not averages.

Your benefits advisor and TPA should be active partners throughout this process. Roundstone’s CSI team can help model cost scenarios and identify which network configurations have performed best for similar member populations.

The Network Is a Plan Design Decision

Self-funding plans require a different mindset from traditional, fully insured plans. With self-funding, provider network selection is a plan design decision. The network you choose determines where your employees get care, what it costs the plan, and what it costs them.

In a group captive structure, where claims transparency and cost control are the point, a misaligned network undermines everything else.

Getting it right takes data, a clear picture of your workforce, and experienced partners who can translate both into a recommendation.

With Roundstone, you get all of that and more.

To learn more about choosing a provider network, see our Frequently Asked Questions below.

Why Roundstone?

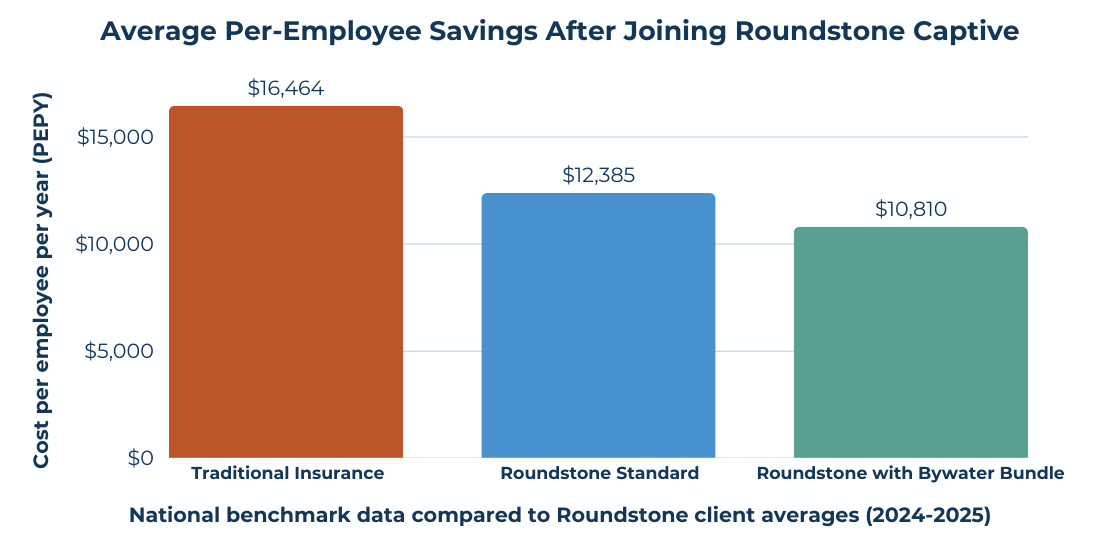

Roundstone members average $12,385 per employee per year versus the industry benchmark of $16,464. Members on the Preferred Bundle average $10,810; that’s 34% below benchmark.

Roundstone has returned $91.8 million in unused premiums to captive members to date, and backs every membership with a five-year savings guarantee.

The right network, matched to your workforce and administered by a TPA that shares your goals, directly affects what your plan costs and how employees experience it. The Preferred Bundle is a proven starting point. If you have your own network, bring it. Flexibility is part of the model by design.

Contact Roundstone today to learn how to create your own self-funded health insurance plan.

Frequently Asked Questions: Choosing a Provider Network for a Self-Funded Health Plan

Broad networks contract with a large percentage of local providers; narrow networks trade choice for better-negotiated rates. Self-funded employers can build tiered structures that offer employees both options at different cost-sharing levels.

Unlike fully insured plans, self-funded health plans give employers complete freedom to contract with any network that fits their workforce. You can also layer specialty arrangements like Centers of Excellence on top of a broader network.

National provider counts mean little if coverage is thin near your workforce. Ask vendors to map in-network providers against your employees’ home zip codes before committing.

Network adequacy measures whether employees can actually access in-network care in a timely way. When they can’t, out-of-network claims drive up plan costs and undermine your cost containment strategy.

Benchmark reimbursement rates against Medicare, not billed charges, because billed charges are arbitrary and easily manipulated. Ask networks for rate data on your most common procedure codes specifically.

It sets plan reimbursement based on an objective benchmark, typically a Medicare multiplier, rather than arbitrary network discounts. It can significantly reduce facility costs and is one of the most effective cost containment strategies available to self-funded employers.

One of the core advantages of self-funded health insurance is the ability to change network vendors without restructuring your underlying plan. You can also add specialty arrangements mid-year without disrupting overall plan design.

Your claims data tells you which specialties employees use most, which facilities they visit, and where costs are concentrated, all of which should drive the network decision. Roundstone Reporting gives group captive members direct access to that information.

Most self-funded plans cover out-of-network care at a higher cost-sharing level, and the No Surprises Act provides protections against balance billing for emergency services. Your TPA and plan documents govern how those claims are processed.

Roundstone’s Preferred Bundle pairs the Cigna national network with Bywater TPA and select transparent PBMs, delivering an average of $1,700 less per employee annually versus other configurations. Group captive members who prefer a different network can bring their own, because flexibility is built into the model.

PBM selection is the primary lever. Traditional PBMs profit from spread pricing, the gap between what they charge your plan and what they pay the pharmacy, which is invisible in a fully insured arrangement. Roundstone’s Preferred Bundle includes transparent, pass-through PBMs that show ingredient costs at the transaction level, so self-funded employers manage pharmacy spend rather than absorb it.

Advisory Board. “How Employers Are Using Centers of Excellence Networks to Cut Costs.” Advisory.com, Feb. 14, 2020. https://www.advisory.com/blog/2020/02/employer-centers-of-excellence-networks

Business Group on Health. “2025 Large Employer Health Care Strategy Survey: Executive Summary.” businessgrouphealth.org, 2025. https://www.businessgrouphealth.org/resources/2025-employer-health-care-strategy-survey-executive-summary

Herman, Bob. “Employer Health Costs to Rise Again in 2025, Aon Projects.” Healthcare Dive, 2024. https://www.healthcaredive.com/news/employer-healthcare-costs-increase-2025-aon/724505/

KFF. “2025 Employer Health Benefits Survey.” kff.org, 2025. https://www.kff.org/health-costs/2025-employer-health-benefits-survey/

ABOUT THE AUTHOR

Roundstone Team

Enjoy Reading?

Check out these similar posts.

How to Choose a Provider Network for a Self-Funded Plan

How to Compare PBMs: A Practical Evaluation Framework

Roundstone Insurance © 2025