- Employers

- Advisors

ADVISORS

Roundstone recognizes and appreciates the important role benefits advisors play — that’s why we only operate through our network of trusted advisors.

- Resources

THE LATEST AND THE GREATEST

- Blog

BLOG

Stay up-to-date with the latest trends and learn about how small to midsize businesses can enjoy the benefits of self funded health insurance.

LATEST POST

FEATURED FAVORITES

- About Us

ABOUT US

We are a health benefits captive providing self-funded solutions to small and mid-sized employers. Our self-funded medical group captive bands employers together to fund their benefits the way much larger Fortune 500 companies do.

- Our TPA

TOPIC

How to Compare PBMs: A Practical Evaluation Framework

- Roundstone Team

- 8 Minute Read

- Category Here

Find this article helpful? Share it with others.

Pharmacy costs are rising faster than almost any other line item in your health plan. Specialty drugs, GLP-1 medications, and brand-name biologics are pushing per-employee drug spend to levels that felt unthinkable five years ago.

Yet, most employers still select their pharmacy benefit manager the same way they always have: They take whoever the carrier or third-party administrator (TPA) hands them, sign a contract they don’t fully understand, and assume the arrangement is roughly fair.

A KFF Health News report found that most employers have little idea what their PBM does with rebate dollars. Gary Claxton, a senior vice president at KFF and leader of the survey, warned that “employers are generally frustrated by the lack of transparency into all the prices out there. They can’t actually know what’s true.”

That information gap translates directly into dollars left on the table, and the only way to close it is through a more intentional, hard‑nosed PBM selection process.

PBM Cost Savings and the Cost of Getting It Wrong

Pharmacy benefits typically represent 15 to 25 percent of total health plan costs, and that share is climbing as specialty prescription drug use expands. How your PBM generates revenue has a direct bearing on what you pay. Many employers discover this detail only when they start asking questions their PBM would prefer they didn’t.

Traditional PBMs make money through spread pricing, meaning they charge your plan more for a drug than they pay the pharmacy and pocket the difference. They also retain a portion of manufacturer rebates negotiated on your behalf.

A 2025 Pharmaceutical Strategies Group survey found that only about 60 percent of employers receive 100 percent of their rebates. The other 40 percent are funding their PBM’s profits without knowing it.

Pharmacy Benefit Manager Evaluation Starts With the Business Model

The three basic PBM structures produce meaningfully different outcomes for your plan. Below is a simple comparison.

Roundstone recommends transparent and pass-through models for all group captive members. The reason is structural: A spread-pricing PBM earns more when drug costs are higher. That’s an incentive problem worth taking seriously, especially in specialty drugs, where the margins on a single medication can run to thousands of dollars per fill.

For a fuller explanation of how these models work day-to-day, see our overview of pharmacy benefit managers and self-funded plans.

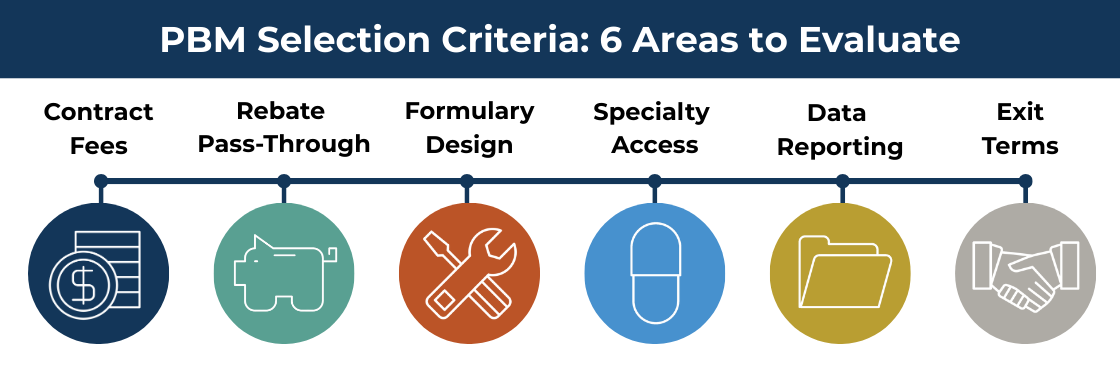

PBM Selection Criteria: What to Examine Before You Sign

A useful PBM comparison goes well beyond comparing per-prescription admin fees. These are the areas that reveal whether a vendor will actually work in your plan’s interest, and where weak contracts tend to cost employers the most.

Contract Transparency and Fee Definitions

PBM contracts vary considerably in how they define compensation. Some clearly list every fee the vendor collects. Others bury figures in definition clauses or leave them undefined.

Ask for a draft contract early and have someone read the entire contract carefully, not just the summary sheet. If a vendor is reluctant to provide contract language before you’ve committed, that hesitation is informative.

Key questions to ask about contract structure:

Does the contract define all administrative fees, clinical program charges, specialty pharmacy margins, and any spread retained on generics?

Are fee definitions written with enough specificity to audit?

Can you negotiate terms directly? Self-funded employers have leverage here that fully insured employers don't. See our cost containment overview for what to look for.

Before signing a contract, learn what your fully insured carrier doesn’t want you to know.

Rebate Pass-through and Rebate Aggregators

Manufacturer rebates are negotiated using your plan’s drug volume, so in any reasonable accounting, that money belongs to you. Whether you actually receive it depends entirely on your contract, and pass-through rates frequently differ between traditional and specialty drugs. Ask about both.

One detail worth pressing on: Some large PBMs now route rebate negotiations through offshore entities or group purchasing organizations. This structure lets them capture a portion of the rebate before it reaches the PBM’s own books. The practice has attracted regulatory attention but is still common enough to ask about directly.

Questions to bring to the conversation:

Are rebates passed through at 100 percent for both traditional and specialty drugs?

Does the PBM use a rebate aggregator or offshore group purchasing entity? If so, what portion of rebates flows through that entity before reaching your plan?

Get the rebate commitment in writing.

Join Our Newsletter

Sign up for fresh insights straight to your inbox.

Formulary Design and Clinical Independence

You can build your formulary (drugs your plan will cover) around clinical outcomes or around rebate maximization. A high-rebate drug is often a high-list-price drug, and a formulary optimized for the PBM’s rebate revenue may place expensive branded medications in preferred tiers while pushing lower-cost alternatives toward higher out-of-pocket costs.

Our overview of how captive members save on prescription drug prices covers how these decisions play out in practice.

Ask your prospective PBM:

Who makes formulary placement decisions, and is there an independent clinical committee involved?

How are preferred tiers assigned: by therapeutic outcomes, rebate economics, or some combination?

How frequently is the formulary reviewed, and what triggers a change?

Benefit advisors: Learn how to offer your clients the cost-saving benefits of a PBM they choose.

Specialty Pharmacy Access

Specialty drugs, including biologics, oncology medications, and certain infusion therapies, are where pharmacy spend gets large fast. Most major PBMs own specialty pharmacies, and some contracts require your employees to use them exclusively.

That’s a conflict worth scrutinizing: The PBM earns a dispensing margin regardless of whether the affiliated pharmacy offers competitive pricing.

Ask whether your plan can access independent specialty pharmacies and under what conditions.

If the contract requires exclusive use of an affiliated specialty pharmacy, understand what that restriction costs you in terms of negotiating power.

Pharmacy Data Access and Reporting

You should be able to see actual drug costs paid, rebates received, generic dispensing rates, and specialty drug utilization without having to request a custom report or wait for a quarterly review.

If the PBM’s reporting makes it difficult to reconcile what you’re paying against what the contract says you should pay, that’s worth investigating before you’re a year into the relationship.

Self-funded employers in Roundstone’s captive get this visibility through Roundstone Reporting, which puts pharmacy and medical claims side by side in a format built for decision-making, not compliance filing.

Ask about:

How frequently reporting is available and in what format

Whether you can reconcile rebates received against contract terms without requesting a special audit

What happens to your data if you leave the PBM and whether it can it be exported in a usable format

Exit Terms and Data Portability

Lock-in provisions, high termination fees, and data portability restrictions all deserve attention before you sign. A PBM with a multi-year lock-in and limited data portability is one that knows the relationship won’t hold up to ongoing scrutiny.

That’s not necessarily a disqualifier, but know up front what leaving would cost you and whether your claims history can actually be extracted if you decide to switch.

Pharmacy Benefit Manager Mistakes That Cost Employers Most

The evaluation criteria above assume you’re starting from scratch. In practice, most employers make one of a few predictable mistakes that leave money in the system.

Treating the Admin Fee as the Whole Story

The most common error is evaluating based on admin fee alone. A per-prescription fee that looks competitive might be paired with aggressive spread pricing on generics or low rebate pass-through on brand drugs.

The only figure that matters is net pharmacy cost after all fees and rebates are accounted for, and most PBMs don’t hand that number over without being pushed.

Inheriting a PBM Without Evaluating It

Many employers move to a self-funded plan, accept the PBM their TPA recommends, and never revisit the decision. Before accepting a TPA’s preferred vendor, ask directly whether the TPA receives any compensation from that PBM.

The arrangement may be completely legitimate, but you want to understand the incentive structure before you rely on the recommendation.

Skipping the Formulary Review at Renewal

Formulary reviews tend to get skipped at renewal, even when the rest of the plan gets scrutinized carefully. Drug mix shifts over time, new specialty medications get added, and what was a reasonable formulary two years ago may now be steering employees toward higher-cost options.

Building an annual review of generic dispensing rates and specialty utilization trends into your renewal process is worth the effort.

Letting the Relationship Drift

Even a well-structured PBM relationship can slip over time as rebate negotiations shift and plan composition changes. Roundstone’s Partner Solutions team performs this kind of ongoing review as part of standard plan management for captive members. The team compares actual rebates received against contract terms and flagging trends before they compound, and reports them to you.

CFOs: Self-funding saves money. Learn how much and how to make it work for your company.

Self-Funded PBM Selection: Why You Have More Options Than You Think

Employers in a group medical captive get to choose their PBM. That may sound like a small thing until you consider what it means in practice. A fully insured employer accepts whatever vendor the carrier assigns, selected based on the carrier’s economics.

Self-funded employers own their plan design and can select vendors based on their own criteria, which makes the evaluation process described above worth doing carefully.

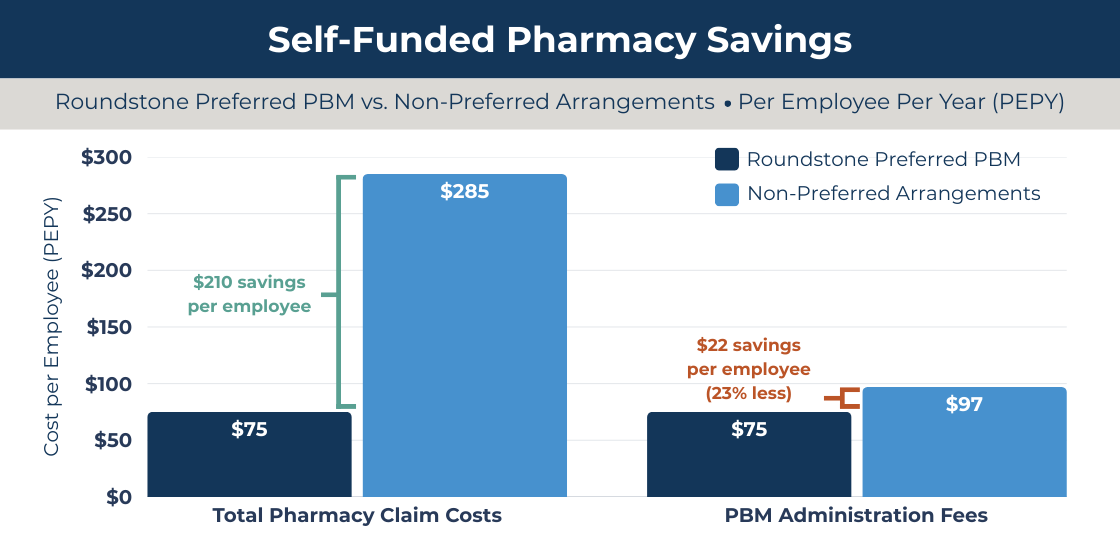

The financial difference is measurable. Roundstone’s preferred PBMs deliver total pharmacy claim costs that average $210 less per employee annually compared to non-preferred arrangements. The gap compounds across a workforce over multiple plan years.

That result comes from selecting PBMs with transparent fee structures, full rebate pass-through, and formulary designs that aren’t optimized around the PBM’s own rebate revenue.

Self-funded Pharmacy Savings Depend on Vendor Freedom

The structure of your self-funded plan matters here. Some TPAs restrict your choice of vendors, either through preferred arrangements or contractual requirements. If your TPA limits PBM options, your advisor should evaluate those options independently to confirm they deliver savings to the plan and not just additional compensation to the TPA.

Source: Roundstone Insurance internal data

Savings reflect aggregated internal analysis of Roundstone captive groups comparing preferred PBM arrangements to non-preferred configurations on a per employee per year (PEPY) basis. Results vary by employer and are not guaranteed. Contact Roundstone for methodology details.

Why Work With Roundstone?

When you work with Roundstone, the results are measurable. Roundstone has returned $91.8 million in unused premiums to captive members, preferred PBMs deliver $210 less per employee annually in total pharmacy claim costs, and mature plans renew at 3 to 5 percent on average. The Roundstone Guarantee backs it all: savings within five years, or we make up the difference.

Learn More About Choosing Your Own Pharmacy Benefits Manager

At Roundstone, we’re all about options. Here’s how you can learn more:

Watch the Webinar

Our on-demand PBM evaluation webinar walks through the full scorecard process with real contract examples, including how to read a rebate pass-through clause and what to ask about specialty pharmacy arrangements.

Watch How to Pick the Right PBM.

Get the eBook

Our free eBook “Strategies to Contain the Rising Cost of Pharmacy” is a detailed look at the cost-containment measures available to Roundstone group captive members.

Contact a Roundstone Rep

The questions in this article are ones fully insured employers often can’t get answered because the carrier controls all vendor relationships. Self-funded employers in Roundstone’s group captive choose their own PBM, see their own claims data, and work with our Partner Solutions team to review pharmacy performance year-round, not just at renewal.

Contact Roundstone to request a proposal and see what your pharmacy spend could look like with the right vendor in place.

Claxton, Gary, et al. “Employers Haven’t a Clue How Their Drug Benefits Are Managed.” KFF Health News, Oct. 9, 2024, kffhealthnews.org/news/article/employer-drug-benefits-pbms-survey-kff/

KFF (Kaiser Family Foundation). “2023 Employer Health Benefits Survey.” Oct. 2023, kff.org/health-costs/report/2023-employer-health-benefits-survey/

KFF (Kaiser Family Foundation). “2024 Employer Health Benefits Survey.” Oct. 2024, kff.org/health-costs/report/2024-employer-health-benefits-survey/

KFF (Kaiser Family Foundation). “2025 Employer Health Benefits Survey.” Oct. 22, 2025, kff.org/health-costs/report/2025-employer-health-benefits-survey/

Mintz. “PBM Policy and Legislative Update — Summer/Fall 2025.” Mintz, Nov. 4, 2025, www.mintz.com/insights-center/viewpoints/2025-11-04-pbm-policy-and-legislative-update-summer-fall-2025.

Pharmaceutical Strategies Group. “2025 Trends in Drug Benefit Design Report.” Drug Channels, 2025, www.drugchannels.net/2023/08/surprising-data-on-employer-pbm-rebate.html.

ABOUT THE AUTHOR

Roundstone Team

Enjoy Reading?

Check out these similar posts.

Roundstone Insurance © 2025