- Employers

- Advisors

ADVISORS

Roundstone recognizes and appreciates the important role benefits advisors play — that’s why we only operate through our network of trusted advisors.

- Resources

THE LATEST AND THE GREATEST

- Blog

BLOG

Stay up-to-date with the latest trends and learn about how small to midsize businesses can enjoy the benefits of self funded health insurance.

LATEST POST

FEATURED FAVORITES

- About Us

ABOUT US

We are a health benefits captive providing self-funded solutions to small and mid-sized employers. Our self-funded medical group captive bands employers together to fund their benefits the way much larger Fortune 500 companies do.

- Our TPA

Find this article helpful? Share it with others.

With Roundstone, you’re not shopping for plans every year. You’re building a long-term strategy. And your clients can feel the difference.

The Renewal Hike No One Can Explain

Every advisor has been there.

A client calls, frustrated and confused. Their fully insured health plan just came back with a double-digit renewal increase—18%, maybe even 22%. They didn’t change anything. No major new hires. No catastrophic claims. Just another unexplained hike.

Now it’s your job to help them make sense of it.

The problem? Fully insured plans rarely offer a satisfying explanation.

Employers don't receive claims data.

Can't pinpoint what drives a cost increase.

No way to address the issue — just a higher premium.

Most employers—and many advisors—don’t realize that fully insured pricing always looks backward. Carriers don’t just project future risk. Instead, they try to recover last year’s losses.

Most employers—and many advisors—don’t realize that fully insured pricing always looks backward. Carriers don’t just project future risk. Instead, they try to recover last year’s losses.

In a fully insured model, the carrier is trying to recover last year's losses. We look at where our members are going—not what happened last year.

That shift—from reactive to forward-looking underwriting—changes everything. It brings cost stability, plan flexibility, and long-term client satisfaction.

Join Our Newsletter

Sign up for fresh insights straight to your inbox.

Case Studies: What Forward Thinking Looks Like

Forward-looking underwriting sounds great, but more importantly, it works. Two examples show how this approach drives real savings.

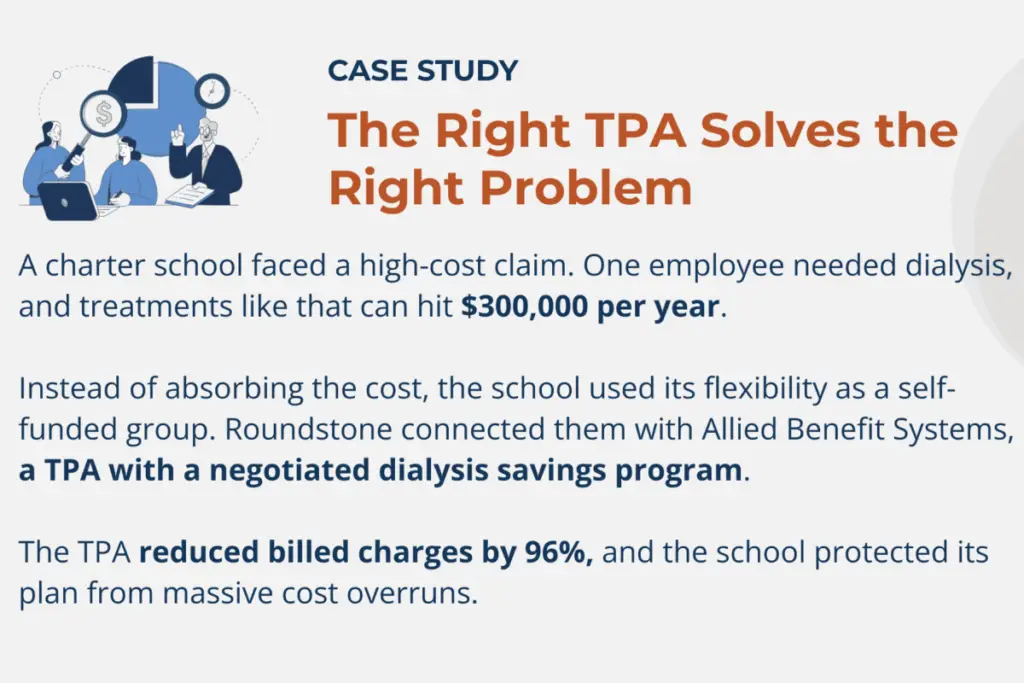

In this success story, instead of carrying a major cost into future renewals, the employer recognized a cost containment opportunity and solved the problem—fast.

In this case, we saw a problem, so we matched the group with a TPA who could solve it. That’s the kind of targeted solution you can only offer when you have control of your healthcare plan.

The employers in these examples didn't accept inflated renewals. They used data, insight, and choice to protect their plans—and their budgets.

From Reactive to Strategic: The Advisor's Role in the Shift

Advisors who guide clients into a self-funded group captive save them money—and change the entire conversation.

Fully insured plans force employers into a reactive cycle:

Wait for the renewal.

Brace for the increase.

Shop around — again.

That’s not strategy—it’s damage control. And it happens every year.

When you work with a group captive that applies forward-looking underwriting, you help your clients break the cycle. You show them how to:

Use data to find cost drivers before they get out of hand.

Solve problems instead of deferring them.

Use data to find cost drivers before they get out of hand.

Advisors who make this shift become more than brokers. They become allies—professionals who bring insight, clarity, and control to one of the most frustrating costs businesses face.

Let Go of the Past—and Lead Your Clients Forward

Health insurance doesn’t have to be a mystery.

When employers stop relying on backward-looking pricing, they gain more than savings. They gain control. And when you guide them through that shift, you elevate your value as an advisor.

Most groups can self-fund—they just need the right model and the right partner. You don't need to take on more risk. You just need to stop playing by outdated rules.

Fully insured plans will keep raising premiums without showing their work. Forward-looking underwriting changes that. It offers:

Transparent data

Predictable pricing

Real strategies to reduce spend

The group captive model gives you a framework for long-term success. You’re not trying to outguess the next renewal. You’re helping clients make confident, informed decisions about their health plans—before problems arise.

This isn’t just about saving money. It’s about making your healthcare plan smarter.

If your clients keep paying for last year’s claims, show them a better path forward. Talk to a Roundstone Regional Practice Leader today.

ABOUT THE AUTHOR

Ian Woidke

Enjoy Reading?

Check out these similar posts.

Roundstone Insurance © 2025