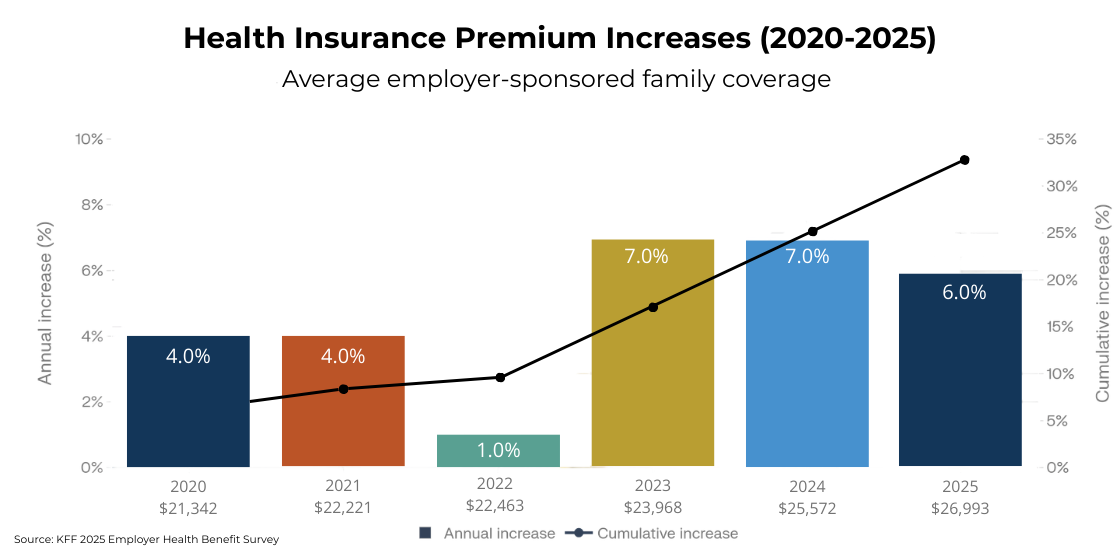

As employer healthcare costs continue to climb, the pressure is no longer manageable through small plan tweaks. The average annual premium for employer-sponsored family coverage reached $26,993 in 2025, and employers are questioning whether traditional network-based plans still deliver value.

Many are exploring alternatives that promise more control and lower costs. Reference-based pricing (RBP) is one of those options. It offers a different way to pay for care, one that replaces negotiated network rates with a fixed pricing model tied to Medicare.

RBP can reduce costs in the right situations, but it also introduces new risks that employers need to evaluate carefully. This article explains how reference-based pricing works, where it delivers value, where it creates challenges, and how a group captive structure builds on the same principles while addressing the gaps.

What Is Reference-Based Pricing?

Reference-based pricing is a reimbursement model that sets a fixed payment amount for medical services based on a benchmark, typically a percentage of Medicare reimbursement rates.

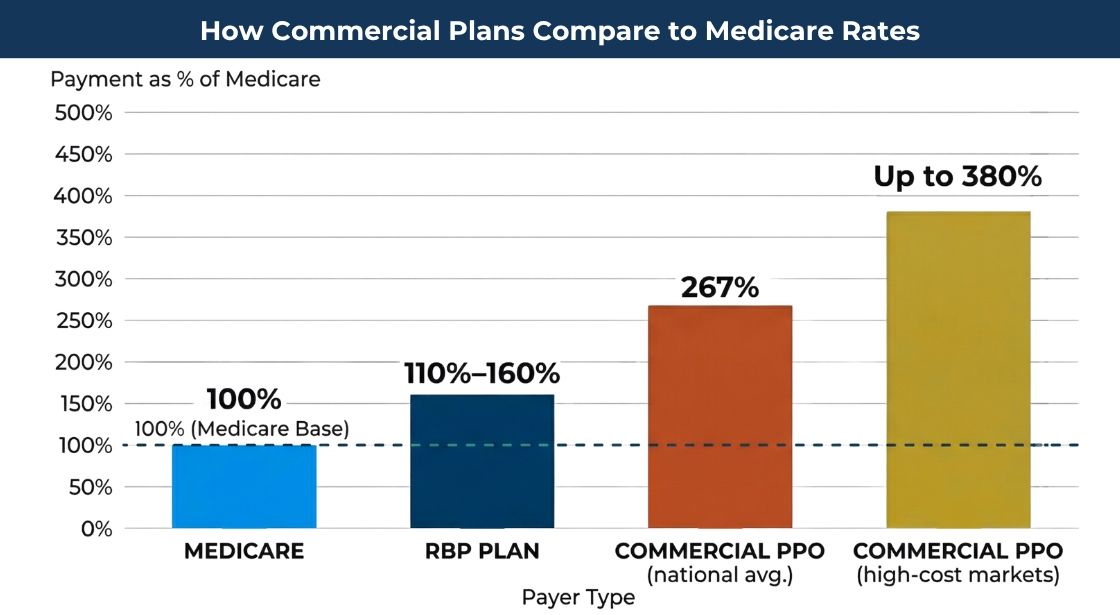

Instead of relying on a provider network to negotiate discounts off billed charges, an RBP plan pays a defined percentage of Medicare rates. Most plans fall between 110% and 200% of Medicare, depending on the service and market conditions.

This creates a clear pricing structure. Medicare rates are public and standardized, which means employers know what they’re paying and why.

Traditional PPO plans take a different approach. They advertise discounts off provider charges, but those charges often start at inflated levels. It is common for PPO plans to pay significantly higher percentages of Medicare rates once the “discount” is applied.

The result is a pricing gap that many employers are starting to question.

How Reference-Based Pricing Works in Practice

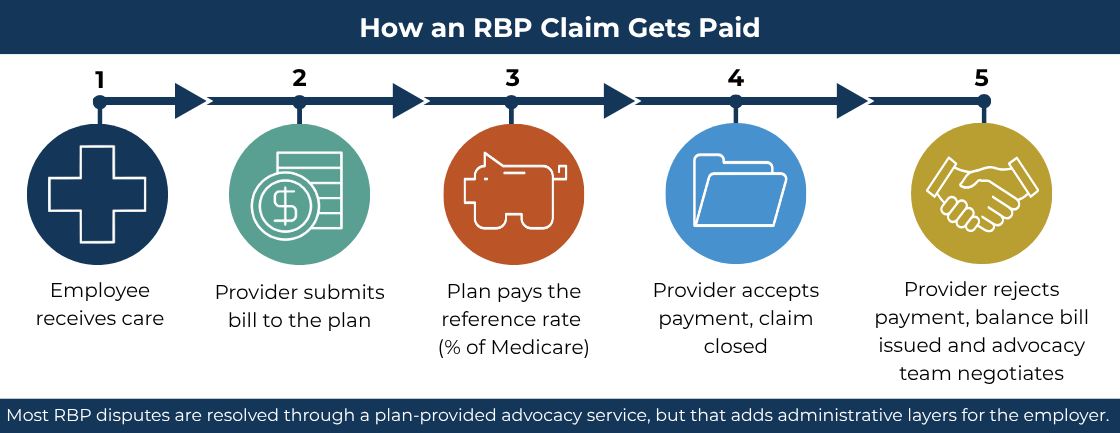

Reference-based pricing changes how claims are paid, but the overall flow of care remains familiar.

An employer adopts an RBP model through a third-party administrator (TPA) or specialized vendor. The plan sets reimbursement limits for categories such as inpatient hospital stays, outpatient procedures, and physician services. These limits are expressed as a percentage of Medicare rates.

When an employee receives care, the provider submits a bill to the plan. The plan pays the predetermined reference rate. If the provider accepts that payment, the transaction is complete.

The complexity shows up when a provider doesn’t accept the payment.

In those cases, the provider may issue a balance bill to the employee for the difference between their charge and the plan’s payment. This creates a dispute that must be resolved through negotiation or advocacy support.

Many RBP plans include an advocacy service to handle these situations, but it adds another layer of administration and requires coordination between the employer, the TPA, and the employee.

Where Reference-Based Pricing Delivers Real Savings

Reference-based pricing can produce meaningful savings when applied in the right areas.

Facility costs are the primary opportunity. Hospital billing represents a large share of total healthcare spend, and Medicare-based pricing can significantly reduce what employers pay for inpatient and outpatient services.

The model also improves pricing clarity. Employers can see the reimbursement formula and understand how each claim is calculated. This makes financial planning more predictable.

RBP also removes the requirement to stay within a provider network. Employees have broader theoretical access to providers, which can be valuable in certain markets.

These advantages appeal to employers who want a more transparent and disciplined approach to healthcare spending.

The table below is a well-documented industry example. RBP saves $22,500 vs. the PPO rate on this procedure, a 50% reduction.

Same Procedure, Three Very Different Price Tags

| Payment Model | How Price Is Set | Amount Paid |

|---|---|---|

|

Hospital billed charge |

Set by chargemaster |

$75,000 |

|

PPO (after 40% “discount”) |

Discount off billed charge |

$45,000 |

|

RBP (at 140% of Medicare) |

Percentage of Medicare rate |

$22,500 |

The Real Drawbacks of Reference-Based Pricing

Reference-based pricing works, but it shifts responsibility in ways that employers need to be prepared for.

Balance billing is the most significant concern. When providers reject the reference payment, employees can receive unexpected bills. Even with advocacy support, these situations create confusion and frustration.

Provider acceptance varies by market. Some hospitals and health systems are more willing to work with RBP plans than others. In areas with limited competition, providers may refuse Medicare-based payments altogether.

The administrative burden increases. RBP plans often rely on advocacy teams to negotiate disputes, answer employee questions, and manage provider communication. That support is necessary, but it adds cost and complexity.

RBP also doesn’t address risk on its own. A large claim still flows directly to the employer unless the plan is paired with stop-loss coverage. The pricing model reduces unit cost, but it doesn’t protect against volatility.

| Challenge | What It Means in Practice |

|---|---|

|

Balance billing |

Providers who reject the reference rate can bill employees directly for the difference |

|

Market variability |

Provider acceptance rates vary — lower in concentrated markets with limited competition |

|

Administrative burden |

Advocacy services are necessary but add cost and coordination complexity |

|

No built-in risk protection |

RBP reduces unit cost but doesn’t limit employer exposure to catastrophic claims |

How Reference-Based Pricing Fits into a Self-Funded Health Plan

Reference-based pricing is a cost containment strategy within a broader self-funded health insurance plan.

A self-funded plan gives employers control over how claims are paid, which vendors are used, and how benefits are designed. RBP is one option for managing the price of care within that structure.

Other cost containment strategies include pharmacy benefit management, wellness initiatives, direct primary care arrangements, and data-driven plan adjustments using detailed claims reporting.

This distinction matters. RBP addresses pricing. It does not solve for risk, data visibility, or long-term plan optimization on its own.

Employers evaluating self-funded health insurance need to think beyond a single tactic and consider how all components of the plan work together.

Self-funding gives employers the structural flexibility to incorporate cost containment tools like RBP, but adoption among small firms remains far below large-employer rates.

How a Group Captive Goes Further Than RBP Alone

A group captive builds on the same goal as reference-based pricing. It reduces healthcare costs through smarter plan design. It also adds the structure needed to sustain those savings.

In a group captive, employers pool risk with other companies. This creates financial protection against large claims while preserving the flexibility of a self-funded model.

Stop-loss coverage is built into the structure, which limits exposure to catastrophic events. That protection isn’t inherent in a standalone RBP strategy.

Data transparency is another key difference. Roundstone provides access to detailed claims data through Roundstone Reporting, giving employers the ability to identify trends, adjust plan design, and take action based on real utilization patterns.

Plan design flexibility allows employers to incorporate multiple cost containment strategies, including reference-based pricing when appropriate. The plan can be tailored to the workforce, the market, and the company’s financial goals.

There is also a financial return component. Roundstone has returned $91.8 million in unused premiums to members. That outcome reflects disciplined plan management and aligned incentives across the captive.

Employers in a group captive often see meaningful healthcare cost savings compared to fully insured plans, with the added benefit of long-term stability.

RBP Alone vs. Group Captive: What Each Delivers

| Feature | RBP (Standalone) | Group Captive |

|---|---|---|

|

Reduces unit cost of care |

Yes |

Yes |

|

Transparent pricing benchmark |

Yes |

Yes |

|

Stop-loss protection |

No — requires separate coverage |

Built in |

|

Claims data access |

Varies by TPA |

Detailed, employer-level reporting |

|

Return of unused premiums |

No |

Yes — Roundstone has returned $91.8M to members |

|

Plan design flexibility |

Limited to RBP methodology |

Full customization across strategies |

Is Reference-Based Pricing Right for Your Company?

Reference-based pricing can be effective, but it is not the right fit for every employer. We recommend the following

Start by understanding your current cost structure. Your per employee per year (PEPY) spend provides a baseline for comparison and helps determine whether pricing or utilization is driving your costs.

Consider your workforce. Some employee populations are more sensitive to provider disruption and balance billing risk than others. That factor should influence any decision involving RBP.

Evaluate your administrative capacity. RBP requires active management, whether through a TPA or an advocacy partner. Employers need to be comfortable with that level of involvement.

Finally, decide what you are trying to solve. If the goal is to reduce unit pricing for specific services, RBP can help. If the goal is to create a sustainable, long-term cost containment strategy with risk protection and data visibility, a group captive offers a more complete solution.

Reference-based pricing works best as one component of a broader strategy. Within a group captive, it can be used alongside other tools to control costs without increasing friction for employees.

The right approach depends on your data, your workforce, and your willingness to manage the tradeoffs. The employers who see the best results are the ones who evaluate these factors upfront and build a plan that fits their reality.

Why Roundstone Members Don't Have to Choose Between Savings and Stability

Reference-based pricing solves one problem well: it brings facility costs closer to a defensible benchmark and gives employers more visibility into what they’re paying. For a plan stuck overpaying under a traditional PPO, that matters.

But pricing discipline alone doesn’t protect you from a catastrophic claim, and it doesn’t return money to your bottom line when your population stays healthy. That’s the difference between a cost containment tactic and a cost containment strategy.

Roundstone’s group captive is built around the latter. RBP can be one tool within the plan, applied where it makes sense for your workforce and market. Alongside it, you get built-in stop-loss protection, employer-level claims data through Roundstone’s Cost Saving Investigators Team, and a structure designed to improve over time.

Roundstone has returned $91.8 million in unused premiums to members, because when every piece of the plan works together, the savings compound.

If you’re evaluating RBP as a way to control costs, that’s a good instinct. The question is whether you want to pursue it in isolation or as part of a structure built to carry that work further. Contact Roundstone for a personalized look at what that could look like for your situation.

FAQ

Reference-based pricing is a model that sets payment limits for medical services based on a fixed benchmark, usually a percentage of Medicare reimbursement rates, instead of negotiated network rates.

The primary disadvantage is balance billing. Providers who don’t accept the reference payment may bill employees for the difference, which creates disputes and administrative complexity.

Yes. Reference-based pricing can be incorporated into a group captive as one cost containment strategy alongside stop-loss protection, claims data transparency, and other plan design tools.

A PPO relies on negotiated discounts off provider charges. Reference-based pricing ties payments to Medicare rates, which are typically lower and more transparent.