By Ryan Audin, Regional Practice Leader at Roundstone

By Ryan Audin, Regional Practice Leader at Roundstone

Behind every healthcare plan is a high-stakes negotiation that determines whether employers and employees can access affordable, high-quality care. Yet, many employers remain sidelined in these discussions, unaware of how these negotiations unfold and who truly advocates for their interests.

Healthcare negotiations between providers and insurance carriers dictate reimbursement rates, network access, and the overall cost of care. These discussions directly impact an employer’s healthcare expenses, yet many businesses lack the information and influence to drive cost-effective outcomes.

Traditional insurance models keep employers in the dark. Fully insured plans limit transparency, leaving businesses with little control over rising costs. Many brokers, bound by relationships with large insurance carriers, do not always prioritize employer advocacy.

For self-funded employers who rely on cost containment solutions to mitigate cost fluctuations, they have skin in the game. Unlike fully insured businesses, which rely on carriers to absorb cost fluctuations, self-funded companies bear the direct financial impact of these negotiations.

That’s why choosing the right benefits advisor is critical. A knowledgeable, transparent advisor doesn’t just sell you a plan—they equip you with the insights and strategies needed to take an active role in negotiations that affect your costs and employee coverage.

Advisors: Learn more about self-funding through a group captive program.

What’s Being Negotiated—and Why Employers Should Care

Healthcare contract negotiations shape how businesses interact with the healthcare system. Understanding what’s on the table can help employers anticipate changes and develop strategies to contain costs.

Reimbursement Rates and Cost Impact

Reimbursement rates dictate how much insurers pay healthcare providers for medical services, influencing the overall cost structure of an employer’s health plan.

Without fair negotiations, employers may face:

- Higher expenses that drive up employee premiums and out-of-pocket costs

- Reduced coverage options that limit provider access

- Network instability, leading to unexpected out-of-network charges

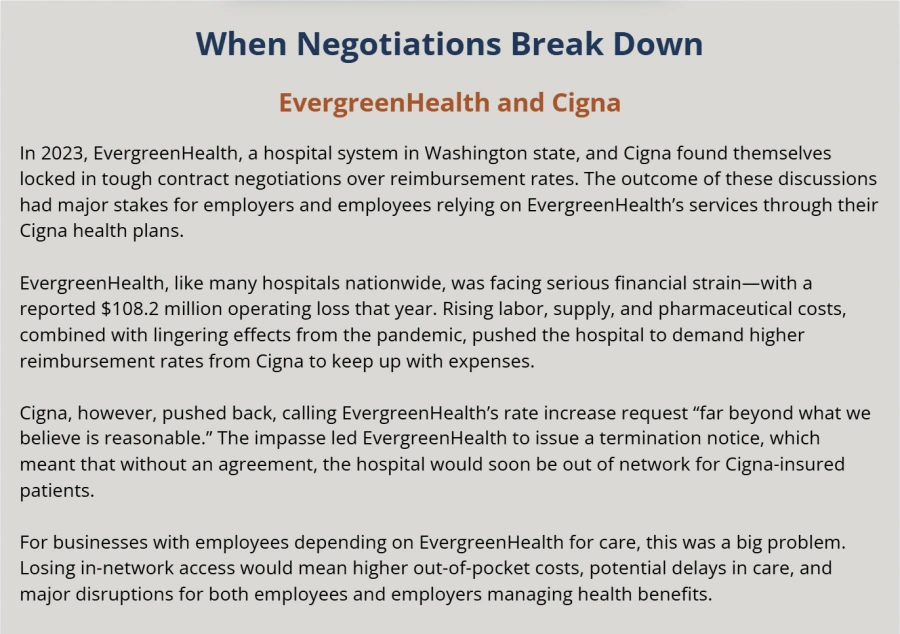

For example, EvergreenHealth’s recent negotiations with Cigna in Washington highlight the financial risks of reimbursement disputes. Employers in that network faced uncertainty over continued in-network access, potentially leading to higher costs for businesses and employees.

The right advisor ensures employers understand how these rates affect their bottom line, helps them anticipate potential disruptions like the EvergreenHealth-Cigna dispute, and provides strategic cost-containment solutions to mitigate financial risk and maintain stable provider access.

Administrative Agreements and Cost Efficiency

Beyond pricing, negotiations cover operational agreements that impact plan administration, including:

- Claims processing speed and accuracy. Delays or inaccuracies drive up employer costs

- Payment schedules for providers. Unfavorable terms can disrupt cash flow and increase financial instability

- Care coordination for high-cost claims. Weak management strategies result in excessive spending

A proactive advisor will help structure a plan that ensures efficiency, cost containment, and uninterrupted care for employees.

Strategic Planning for Cost Control

Savvy employers don’t just accept the terms dictated by carriers and providers—they leverage data and expert guidance to drive negotiations.

A strong benefits advisor will:

- Benchmark reimbursement rates to ensure fair pricing

- Introduce value-based care agreements to reward quality over quantity

- Implement cost-containment strategies using claims data analysis

- Advocate for provider performance standards to ensure efficiency and affordability

Why Employers Lack Power in Negotiations—and How to Change That

Many employers assume they have no role in healthcare negotiations. The reality? Traditional insurance carriers and status quo brokers often keep employers passive to protect their interests.

Here’s what’s holding businesses back:

- Lack of transparency. Most fully insured plans don’t provide claims data, preventing employers from making informed decisions.

- Limited broker advocacy. Some advisors prioritize carrier relationships over employer interests, offering little guidance beyond annual renewals.

- Reactive, not proactive strategies. Employers often adjust to rate increases rather than proactively negotiating better terms.

The solution? Partner with a benefits advisor who works for you—not the insurance companies. An advocate, not just a salesperson.

A consultative advisor will:

- Provide claims transparency so you see exactly where your money is going

- Help you benchmark costs to ensure fair rates

- Guide you through self-funding options that give you more control

- Work year-round—not just at renewal—to optimize cost-saving strategies

How Employers Can Prepare for Healthcare Negotiations

Taking a proactive role in healthcare negotiations can prevent cost spikes, coverage gaps, and unnecessary financial strain. Here’s how the right advisor can guide you:

Best Practices for All Employers

- Set clear goals. Define your ideal cost structure, employee coverage priorities, and acceptable rate ranges before negotiations begin.

- Use market data. Work with your advisor to benchmark reimbursement rates and compare plan options.

- Educate internal stakeholders. Keep HR and finance leaders informed about cost trends and potential negotiation outcomes.

Critical Steps for Self-Funded Employers

- Leverage stop-loss insurance. Protect against catastrophic claims to prevent financial instability.

- Join a group captive. Pool risk with other businesses for greater cost predictability and negotiation leverage.

- Use claims data. Analyze provider costs and employee utilization trends to adjust your plan proactively.

What Happens When Negotiations Fail?

A failed negotiation or terminated contract can have immediate and costly consequences:

- Higher employee costs. Out-of-network charges and limited provider access increase financial burdens.

- Increased employer expenses. Without a favorable agreement, businesses face higher claims costs and administrative fees.

- Plan restructuring challenges. Employers may need to adjust coverage or switch networks, creating disruption.

How Self-Funded Employers Can Mitigate Risk

- Stop-loss insurance. Protects against unexpected cost spikes.

- Captive programs. Offer financial stability by spreading risk among a group of employers.

- Employee communication. Keeping employees informed about network changes minimizes disruptions and complaints.

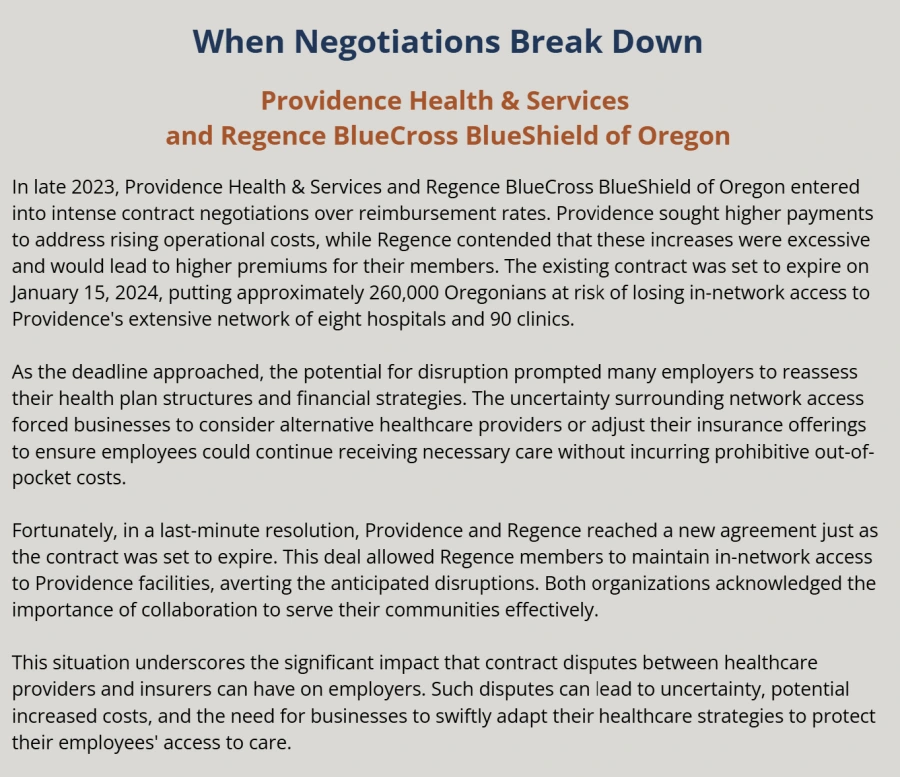

For example, Providence Health’s contract dispute with Regence Blue Cross Blue Shield in Oregon disrupted network access for many businesses, forcing employers to reassess plan structures and financial strategies to manage cost increases.

The Employer’s Role: Be Proactive, Not Passive

Healthcare negotiations don’t just happen to you—you have the power to shape the outcome. Employers who take an active role can:

- Control costs through strategic plan design.

- Improve care quality by aligning with top-performing providers.

- Prevent surprise rate hikes through transparent claims management.

But you don’t have to do it alone. The right advisor will walk you through each step to make sure you’re equipped with the data, leverage, and strategy needed to drive meaningful savings and better outcomes for your employees.

Take Control of Your Healthcare Costs with Roundstone

At Roundstone, we help businesses like yours break free from the constraints of traditional insurance. Through self-funded group captives, we provide:

- Transparent cost-containment strategies

- Stop-loss protections for financial stability

- Access to claims data so you stay in control

Don’t leave your healthcare costs in someone else’s hands. Partner with an advisor who puts you first. Contact Roundstone today to explore how a self-funded group captive can give your business the power to negotiate better healthcare outcomes.