Written by Bruce Dunham, Director of Underwriting at Roundstone.

Quick Answer: Roundstone underwrites all group captive health plans in house as a managing general underwriter. That means employers and advisors get full visibility into how rates are set, direct access to the underwriting team, and a renewal process that starts months before the numbers arrive.

When renewal season arrives in a fully insured plan, it usually goes like this: A number shows up. Nobody explains it. You pay it or you shop. Either way, you start over next year with the same visibility you had before, which is none.

That’s how the model works.

Fully insured carriers set rates, process claims, and control the data. By the time the renewal lands on your desk, the decisions are already made. You have no window into what drove the number and no real leverage to push back.

Self-funded health insurance through a group captive works differently. The data belongs to you, and the underwriting process is visible. When Roundstone does the underwriting in house, the renewal conversation starts months before the number arrives.

Learn how Roundstone’s in-house underwriting process works, what underwriters look at, how renewals get priced and delivered, and what employers and advisors should expect at every step.

What an Underwriter Does

Every health plan starts with a pricing problem: How much will this group cost over the next 12 months? The underwriter’s job is to answer that question accurately enough to set a premium that covers the group’s expected exposure without pricing them out of the captive.

Two companies with the same number of employees can have very different risk profiles depending on the age of their workforce, the industry they’re in, where they’re located, and the health history of their people. Underwriting accounts for all of it.

In a fully insured plan, that analysis happens behind closed doors. The carrier runs the numbers and delivers a final figure. You see the outcome, but the work stays hidden.

In a self-funded captive, you see the formula.

Why In-House Underwriting Is Different

"We don't look in the rearview mirror. We're looking out the windshield."

Most group captives outsource underwriting to carrier partners. Roundstone keeps it in house. As the only group captive that also serves as its own managing general underwriter (MGU), every underwriting decision happens under the same roof as the claims and third-party administrator (TPA) operations run by Bywater.

When a large claim comes in during active underwriting, the claims team knows immediately, and that information reaches the underwriting team the same day. There’s no lag or handoffs between organizations. Your history stays in one system, visible to the people pricing your plan.

That integration shows up at every stage of the plan year.

Fully Insured vs. Self-Funded Group Captive: How the Models Compare

| Stage | Fully Insured Model | Roundstone Captive |

|---|---|---|

|

Underwriting |

Carrier handles internally, employer has no access |

In-house team prices your group with full data visibility |

|

Claims data |

Stays with the carrier; aggregated and inaccessible |

Shared in real time between underwriting and Bywater |

|

Account management |

Little to none; broker may relay information |

Active; account team works from the same data as underwriting |

|

Cost containment |

Not available; carrier absorbs or passes costs forward |

Ongoing programs inform underwriting and reduce future exposure |

|

Renewal |

A number, delivered late, with no explanation |

Full account of every factor that moved the rate, delivered 90-120 days out |

|

Employer recourse |

Accept, negotiate blind, or shop |

informed conversation backed by a year of shared data |

For employers and advisors, that means the underwriting team is reachable. At Roundstone, it’s a team you can get on the phone with. Renewals also move faster when underwriting, claims, account management, and cost containment all operate from shared data and shared systems.

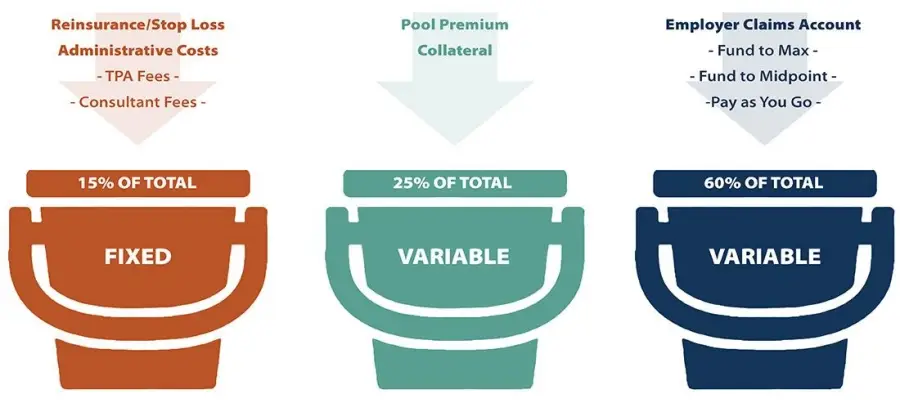

In a self-funded plan, stop-loss insurance is the protection that caps your exposure when claims run high. Your stop-loss premium is what gets underwritten, and it’s built from a specific set of variables.

Roundstone structures total premium into three buckets. The first covers fixed costs: stop-loss premiums, TPA fees, and administrative expenses. These are known quantities that hold for the plan year and represent about 15% of total premium. The remaining 85% is variable, split between pool premium and collateral (25%) and your employer claims account (60%).

The fixed bucket is straightforward to price. The variable buckets are where the underwriting work happens.

Pool premium is priced on your group’s contribution to overall captive exposure. The claims account—the largest bucket at 60%—is the underwriter’s forward-looking estimate of what your group will actually spend on claims over the plan year. Accuracy matters here.

Underwriters look at a specific set of variables to build that estimate, as shown in the table below.

What goes into Stop-Loss Pricing: Group Health Plan Underwriting Factors

| Factor | What It Signals to Underwriters |

|---|---|

|

Demographics (age, gender, family status) |

Baseline utilization expectations and risk concentration |

|

Industry type |

Occupational risk, behavioral health patterns, workforce health norms |

|

Location and network |

Assess to care, unit cost variance, out-of-network exposure |

|

Plan design |

Member cost-sharing, utilization incentives, coverage scope |

|

Specific claims experience |

High-cost claimants, chronic conditions, ongoing treatment patterns |

|

Aggregate PEPM trends |

Direction of overall cost trajectory, rising or falling utilization |

|

Cost containment programs |

Reduced risk profile; supports more competitive claims account pricing |

|

AI Modeling (smaller groups) |

Credibility supplement when claims history is limited |

Aggregate per-employee-per-month (PEPM) trends get close attention. If a group’s costs are rising in a particular area, like specialty drugs, musculoskeletal care, or mental health, that pattern informs the rate.

Active cost containment programs also factor in. If your group has strategies like pharmacy management, direct primary care, or chronic disease programs in place, the underwriter can price the claims account more aggressively because the risk profile is lower.

For smaller groups with limited claims history, Roundstone uses AI modeling to fill credibility gaps, drawing on broader population data to produce a rate that reflects realistic expected costs.

That’s the model working as designed. When claims run lower than projected, unused premiums return to the employer at year end. It’s why Roundstone has returned $91.8 million to its members since 2005.

What Is Shadow Pricing?

Before Roundstone finalizes its renewal number, the underwriting team reviews the incumbent carrier’s renewal in a process called shadow pricing.

The purpose is context. Roundstone builds its number from its own analysis. Shadow pricing adds a layer of understanding about what the existing carrier is signaling about the group’s risk profile.

A large increase from a previous carrier provides real information. If a fully insured carrier is raising a group’s premium by 40% or 60%, the carrier has looked at the claims data and concluded the group is more expensive than the rate it was paying could support.

Roundstone’s analysis may confirm the carrier’s read, or it might reach a different conclusion.

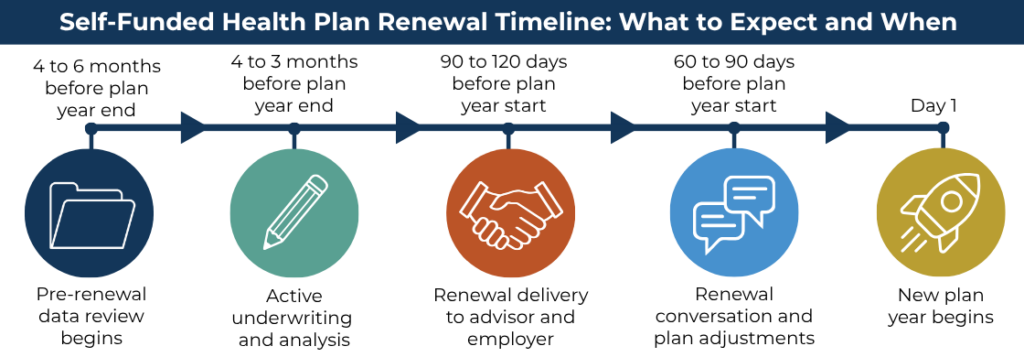

The Renewal Timeline: What To Expect and When

Roundstone begins the pre-renewal process four to six months before a plan year ends. The underwriting team starts pulling claims performance, cost trends, and any developing large claims, and the account management conversation starts at the same time.

The renewal itself is delivered 90 to 120 days before the plan year starts, with a full account of every factor that moved the rate. Employers and advisors walk into the renewal conversation already holding the context.

The question employers ask most often at renewal: “We had a clean year. Why did our premium increase?”

Medical and pharmacy costs rise across the market every year, independent of your group’s claims experience. That trend, currently running at 7% to 8%, shows up in your renewal whether your employees had a good claim year or not.

Pool dynamics matter, too. In a group captive, individual risk is spread across member companies, and a year with significant shared claims affects the pool rate. This shared risk keeps any one employer from having to shoulder a catastrophic plan year on their own.

How Collateral Works and Why It Matters

When an employer joins Roundstone’s captive, collateral is collected at entry. It’s held as security against potential claim obligations, a standard requirement in any self-funded structure.

At Roundstone, that collateral is interest-bearing, collected once on entry to the captive, and returned when the employer exits.

Some competing captive structures collect additional collateral at each new captive close, so obligations stack year over year. An employer in that model might carry $28,000 at year one and $86,000 or more by year five.

In Roundstone’s model, that capital stays accessible to the business. Long-term members rarely face a second collateral call.

Know Your Numbers Before Your Renewal Arrives

Underwriting shouldn’t be a black box, and at Roundstone, it isn’t.

When underwriting, claims, and account management operate as one system, the renewal is the output of a process you’ve been part of all year.

Find out what your group’s numbers look like before the next renewal season hits you with another unexplained premium increase.

Speak to a Roundstone Regional Practice Leader and get started today.

FAQ

What does an underwriter do?

The underwriter’s job is to answer one question: How much will this group spend on healthcare over the next 12 months? That estimate drives the premium. Underwriters analyze workforce age, industry, geography, and claims history to set a rate that covers expected exposure without overcharging.

Why does Roundstone handle underwriting in house?

Roundstone is a managing general underwriter (MGU), so every pricing decision happens internally. That keeps your data in one system, gives the underwriting team same-day visibility into developing claims, and makes them directly reachable to employers and advisors. No handoffs, no lag, no version of your history getting lost between organizations.

What does my premium cover?

Total premium splits into three buckets. Fixed costs (stop-loss premiums, TPA fees, and administrative expenses) make up about 15% and hold steady all year. The remaining 85% is variable: pool premium and collateral at 25% and your employer claims account at 60%, which is the underwriter’s forward-looking estimate of what your group will spend.

How is my claims account calculated?

Underwriters draw on workforce demographics, geographic cost factors, claims history, and aggregate PEPM trends. Active cost containment programs like pharmacy management, direct primary care, and chronic disease management lower the risk profile and allow more competitive pricing. For smaller groups with limited history, Roundstone uses AI modeling to fill credibility gaps with broader population data.

What happens if my group spends less than projected?

Unused funds come back to you. Roundstone has returned $91.8 million to captive members since 2005. Distributions are paid in cash, roughly six to seven months after the policy year closes. You keep every dollar your group didn’t spend.

What is shadow pricing, and why does it matter?

Before finalizing a renewal number, Roundstone reviews the incumbent carrier’s renewal for context. If a fully insured carrier is raising rates by 40% or 60%, that signals how they’ve read the group’s risk. Roundstone’s analysis may confirm that view or reach a different conclusion. Either way, the comparison sharpens the final number.

When does my renewal process start?

Roundstone begins pre-renewal four to six months before the plan year ends, pulling claims data, tracking cost trends, and monitoring developing large claims. The renewal is delivered 90 to 120 days before the new plan year starts, with a full breakdown of every factor that moved the rate.

Why did my premium increase even though we had a clean claims year?

Two factors move rates regardless of your group’s experience. Medical and pharmacy costs rise market-wide each year, currently running at 7% to 8%, and that trend shows up in every renewal. Pool dynamics also matter: a year with significant shared claims across captive members affects the pool rate for everyone.

How does collateral work?

Collateral is collected once at entry, held as security against potential claim obligations, and returned when you exit. It’s interest-bearing. Some competing captives collect additional collateral at each new close, stacking obligations year over year. Roundstone’s model collects it once, so that capital stays accessible to your business throughout your membership.

How is this different from a fully insured renewal?

In a fully insured plan, the carrier controls the data, sets the rate, and delivers a number with no explanation. In Roundstone’s captive, your data belongs to you, the underwriting team is reachable, and the renewal is the output of a process you’ve been part of all year.