TOPIC

Designing Your Group Captive Plan to Cut Costs Your Way

- Roundstone Team

- 6 Minute Read

- Plan Design

Customization Strategies That Work

Customization is where strategy meets execution. These approaches help align plan design with what employees want, while keeping spending under control.

Know Your Workforce

A successful plan starts with knowing who it’s for. Use this data-driven approach to align benefits with employee needs.

Demographics reveal benefit priorities. Age, family structure, and health status influence what matters most, from mental health access to chronic disease support.

Claims data highlights utilization trends. Roundstone Reporting identifies which services drive costs, such as specialist visits or ER use, and suggests solutions like telemedicine or urgent care.

Direct feedback adds critical context. Surveys and focus groups help uncover what employees value, like mental health access or pharmacy convenience.

Preventive care incentives reduce downstream costs. You have the option of lowering copays for routine care, screenings, and disease management to help avoid expensive emergencies and enable early intervention.

You can optimize pharmacy benefits. Transparent pharmacy benefits managers (PBM), smart formularies, and preferred pharmacy networks drive down drug costs while maintaining access to necessary medications.

Behavioral health needs to be accessible. You can reduce copays for therapy, offer telehealth options, and partner with employee assistance programs (EAPs) to improve access and remove stigma.

Wellness programs can be tied to cost-sharing. You can offer HSA contributions or premium discounts for participation in screenings, fitness programs, or smoking cessation.

Plan Design: Vendor Selection Freedom

Employers can choose partners who align with plan design and cost containment goals:

Third Party Administration selection criteria. Choose a TPA that specializes in company size and understand self-funded plan flexibility. Evaluate customer service quality, claims processing speed, and technology platforms.

Pharmacy Benefit Manager partnership strategy. Transparent PBMs pass all savings to plans while traditional models keep significant rebates and fees. Evaluate fee structures, rebate sharing, and formulary flexibility.

Network flexibility. Choose networks based on employee locations and preferences rather than accepting standard carrier options. Regional networks might provide better value for geographically concentrated workforces.

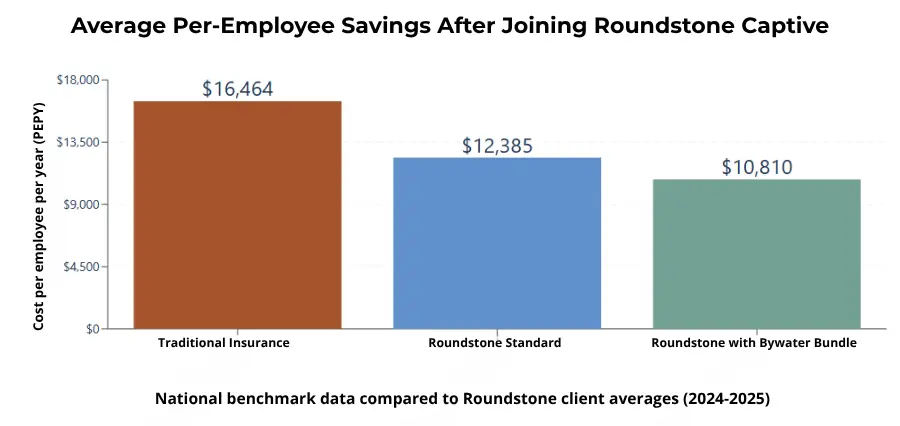

The Roundstone Preferred Bundle. For employers seeking proven vendor integration, Roundstone’s Preferred Bundle combines Bywater TPA, Cigna network, and select transparent PBMs into a coordinated solution.

This strategic combination delivers an average of $1,700 less per employee annually compared to other vendor arrangements, representing 34% savings versus industry benchmarks through seamless integration and optimized cost control.

Plan Design: Implementation and Management

Even the best-designed plan won’t deliver results without effective rollout and oversight. This is where smart planning meets day-to-day management.

Getting Started

Start strong with these foundational steps. A clear budget, realistic timeline, and compliance framework set the stage for a smooth launch.

Budget based on workforce trends. Forecast claims and administrative costs using employee health patterns and demographic insights.

Plan for a thoughtful timeline. Coordinate implementation around existing plan cycles and allow time for vendor onboarding, employee education, and possible phased rollouts.

Meet ERISA requirements. Compliance doesn’t limit customization,but it does require clear documentation and guidance from experienced advisors.

Change Management and Optimization

Communication and continuous improvement are critical. Here’s how to educate employees and fine-tune your plan over time.

Use multi-channel education tools. Combine written guides, digital resources, and live Q&A sessions to explain plan changes and reinforce benefits.

Reinforce what’s staying the same. Employees should know that their ID cards, provider networks, and claims process will remain similar.

Review data regularly. Use quarterly Roundstone Reporting to identify cost drivers and opportunities for improvement.

Track beyond cost. Monitor satisfaction, engagement, and outcomes—not just financials—to ensure the plan is delivering value.

Advanced Plan Design Elements

For experienced self-funders, advanced strategies provide greater control over complex challenges, without sacrificing care quality.

Specialized Benefit Design

Some conditions drive a disproportionate share of healthcare costs. With self-funding, group members can use these design strategies to help manage high-impact needs more effectively:

Target high-cost conditions. Use case management and Centers of Excellence to support employees with chronic conditions or cancer while reducing costs.

Take the pharmacy further. Consider specialty drug management and direct contracts with manufacturers for high-cost prescription medications.

Integrate telemedicine. Build virtual care into your plan with reduced copays for both physical and mental health needs.

Download the free ebook Strategies to Contain the Rising Costs of Pharmacy to learn more about how members of a group captive can save money on prescription medications.

Risk Management and Competitive Advantages

Balance innovation with protection. These techniques help manage risk, stabilize costs, and turn your benefits into a business advantage.

Use stop-loss insurance strategically. Set deductibles that match your cash flow and risk tolerance, supported by captive pooling.

Leverage the captive model. Sharing risk across employers for more aggressive design choices without the individual exposure.

Turn benefits into a differentiator. Tailored plans attract talent and support retention by aligning coverage with employee needs.

Take Control of Plan Design

When employers control plan design, everyone wins. Better benefits, lower costs, and long-term flexibility are all within reach. Group captive self-funding puts employers in charge. With data, transparency, and the right partners, you can build a plan that works for your people and your business.

Assess your current plan. Review claims data, employee feedback, and plan performance to identify customization opportunities.

Build your plan with expert input. Work with Roundstone advisors to design a strategy that fits your budget and workforce.

Plan the rollout. Set timelines, align vendors, and develop your employee communication strategy.

Frequently Asked Questions

A group captive health plan allows multiple employers to pool resources and self-fund employee health benefits, providing more control and customization than traditional insurance. This structure shares risk among participants and often reduces costs.

Cost savings come from customizing benefits to actual employee needs, accessing real claims data, and negotiating with vendors—reducing waste and premium hikes.

Group captives deliver transparency, plan flexibility, vendor control, and the potential for returned unused funds, unlike rigid fully insured plans with higher premiums.

Financial risks are minimized by spreading claims among members and using stop-loss insurance, capping each company’s exposure.

Small to midsize businesses seeking flexibility and long-term savings—especially those frustrated by inflexible, rising costs—benefit most.

Yes, plans can be tailored in areas like copays, networks, and wellness benefits, aligning spending with employee usage.

Employers get detailed claims and utilization reports, enabling proactive decision-making and optimization of health benefits.

Stop-loss and pooled risk coverage protect individual members, but premiums may adjust at renewal if claims run high.

Persistent high claims, nonpayment, compliance issues, or changes in business alignment can result in removal.

Yes, unspent captive funds are often distributed back to members as dividends if claim costs remain low.

Most see value over three years, with returns increasing over time; terms typically require a single-year commitment.

Employers choose third-party administrators, pharmacy benefit managers, and network partners based on organizational needs and cost goals.

Customizable, relevant benefits improve satisfaction and support retention compared to generic, inflexible plans.

It limits each employer’s financial risk by capping payouts on high-cost claims, stabilizing expenses.

Employers receive regular claims and satisfaction reports, allowing them to optimize plan features for better results.

Yes, they must follow ERISA and state insurance guidelines, often with expert advisor support for compliance.

Strategies include targeted case management, specialty pharmacy programs, and telemedicine for chronic disease support.

Enjoy Reading?

Check out these similar posts.